Full Report: Eye on the Last Mile 5.0 - America Edition

Full Report: Eye on the Last Mile 5.0 - America Edition

America Edition

The Industry's First & Only Primary Last Mile Report

The last mile in America is at a tipping point - decisions made today will shape tomorrow’s delivery ecosystem. With expectations rising and markets shifting fast, leaders must balance efficiency, resilience, and innovation. Eye on the Last Mile - USA 2025 is our first primary report capturing this moment. Based on insights from 500+ senior professionals - including C-suite leaders, directors, and heads of transportation, operations, technology, procurement, and compliance - the report uncovers the challenges, priorities, and strategies redefining U.S. logistics.Here are some glimpses of the findings shaping the future of American logistics and supply chains.

Last-mile delivery faces multiple challenges, with cost (18.7%) as the biggest pressure from fuel, labor, and operations. Visibility (13.5%) and carrier performance (11.9%) rank high, demanding transparency and reliable SLAs. Companies seek flexibility (10.9%), better driver management (9.8%), and stronger demand forecasting (9.7%) to handle fluctuations. Enhancing customer experience (9.4%), while building scalability (8.3%) and pursuing sustainability (7.8%), are also critical priorities shaping the future of delivery.

Route inefficiencies, adding up to 20–25% in expenses, remain a top cost driver alongside volatile fuel prices and rising driver labor costs from wage inflation and shortages. Vehicle operating costs grow with aging fleets and supply chain pressures. Lower-ranked but notable factors include ad-hoc carrier use, compliance, order processing, and failed deliveries.

In the US, delivery costs rose an average of 12% from 2024 to 2025, with most increases in the 0–15% range. Some routes spiked 20–30% or even 74%, driven by surcharges or rural fees. Clear clusters at 0%, 10%, and 25% suggest standardized tiered adjustments rather than individualized pricing.

Faster delivery is set to dominate, with same-day and next-day rising from 51% to 62% of shipments by 2027. Same-day grows strongly, while 3–5 day and longer windows shrink. Two–three day delivery remains stable but slightly declines. Retailers must prioritize urban micro-fulfillment, localized inventory, and carrier partnerships as 1–2 day delivery becomes the customer standard.

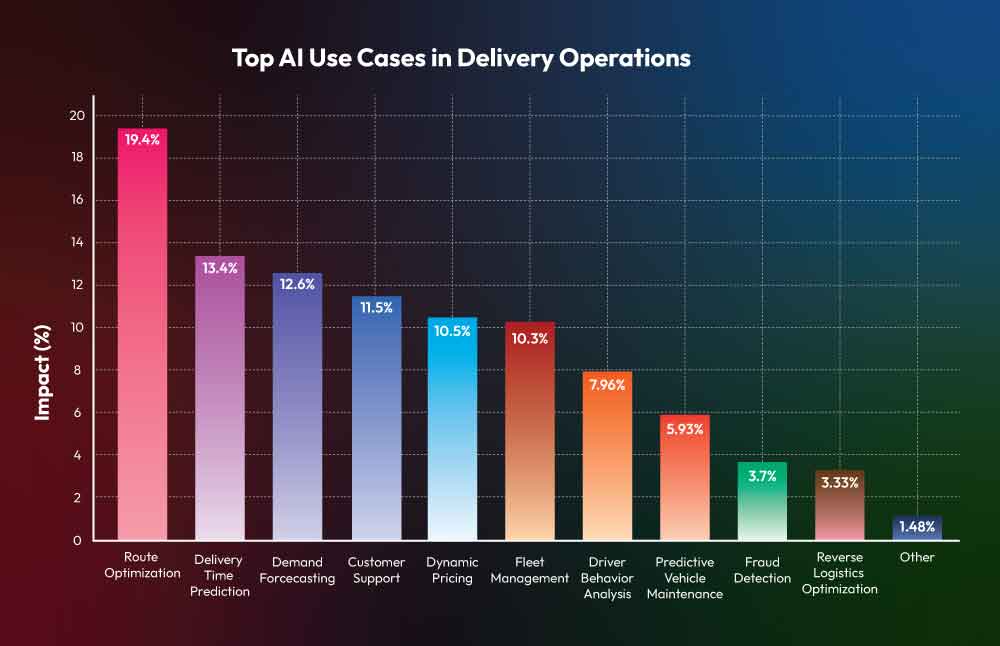

Nearly 43% of companies are in early AI adoption, while 29% are still exploring without clear direction, signaling a need for education and pilots. About 22% haven’t started, citing budget or skill gaps. Just 3.9% have fully embedded AI, and another 3.9% see no relevance yet, highlighting uneven maturity and a widening practicality gap.

Flexibility leads as the top benefit of outsourcing, cited by one-third for enabling quick adaptation to demand and route changes. Scalability and capacity growth follow, representing nearly half of responses, showing value in rapid expansion without heavy investment. Faster delivery (~13%) also matters, while cost reduction (8%) ranks low, highlighting agility over price savings.